Introduction

In its report published in early 1994it advocated the checking from this business into private industry involvement. Ever since that time, there was accelerated growth and talk of insurance in overall cost savings of this market has significantly improved somewhat. Competition on the market is rising with fresh players hoping to set up an important presence. The entire insurance market in India is roughly US$ 30 billion, at the section of FDI is currently US$ 0.5 billion. That is 1.6percent of the overall insurance industry in India. Australian direct investment (FDI) increase in the insurance industry by US$ 0.46 billion in the next two decades and more likely to reach US$ 0.96 billion because it's still regulated.

The relevance of this subject

Currently, just 26 percent of FDI is permitted insurance industry. The entire insurance plan business would reach US$ 60 million in sizes. When an insurance company is opened to an extent of 49 percent for FDIs, then it's estimated that FDI's contribution to the insurer would reach not exactly US$ two billion. Within this paper, we'll analyze the strengths and pitfalls of all FDI in the insurance industry.

AnalysisInsurance and FDI

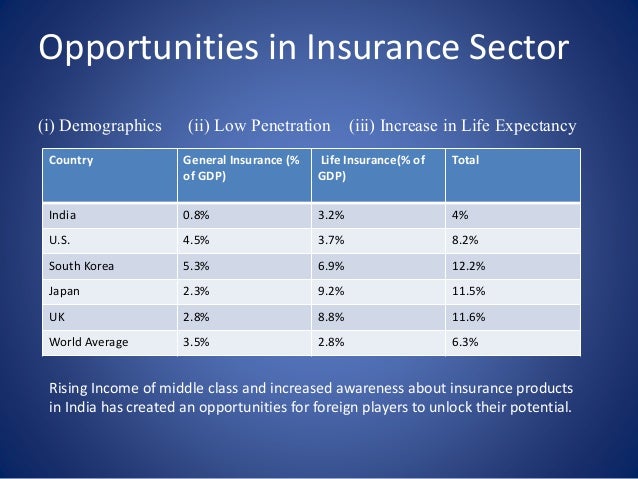

Insurance penetration in India is less than in most East Asian nations. However, the penetration for a percent of GDP has increased from 2.5 from 2005 to 4.0 in 2007 Forever insurance in India

Capital to expansion: FDI has the possibility to meet India's long term funding requirements to invest in the construction of infrastructures that are essential for its maturation of the nation. Infrastructure has become a significant element that includes restricting the improvement of the Indian market. The insurance industry has the ability to increase long-term funding from the masses since it's the sole route where folks devote money for as long as 30 decades more. An upsurge in FDI in insurance could be a blessing for the Indian market, the investments maybe not with standing but by earning more people spend money on long-term capital to fuel the development of the Indian market.

Wider Scope for Growing: FDI in insurance could increase the significance of insurance from India, where the significance of insurance will be abysmally low with insurance top in roughly 3% of GDP percent roughly 8 percent world wide average. This would be better through promotion campaign by MNCs, better product invention, consumer education etc.,.

At just 3.1 percent, India is nicely behind the 12.5percent to Great Britain, 10.5percent to Japan, 10.3percent to Korea and 9.2percent to the United States. Currently, FDI represents just Rs.827 heart of their Rs.3179 crore capitalizations of life insurance businesses.

Provide clients with products that are competitive, more options and superior service levels: Introduction the FDI in the insurance industry could be helpful for most consumers, at a lot of manners. Increasing FDI limitation could affect a lot of businesses in a favorable manner which we might do with no FDI from a Number of Other industries for a few such as in actual estateVikas 2010-11-09T09:38:00

How can it be useful?

The efficiency of those businesses using FDI: The checking of the industry for private involvement in 1999, let the private organizations possess foreign equity up to 26 percent commission. Observing up this 1 2 private industry companies have entered the life insurance industry. Besides the HDFC, that includes overseas equity of 18.6 percent, all of the other private businesses have foreign equity of 26 percent. Generally, insurance private businesses have entered, 6% which may have foreign equity of 26 percent. On the list of personal players generally insurance, both Reliance, and Cholamandalam don't need some foreign equity. The aggregate lack of this life insurance plummeted to Rs. 38633 lakhs compared to this Rs.9620 crores excess (after taxation ) made by the LIC. Generally speaking insurance, 4 from the private insurance suffered declines in 2002-03, with the Reliance, an organization without offshore equity, emerging since the most lucrative player. In reality, the 6 players that are private together with foreign equity made a definite lack in Rs. 294lakhs. On another hand, the people sector insurers generally insurance left aggregate aftertax benefits of Rs. 62570 lakhs.

2. The credibility of foreign businesses: The debate which foreign businesses will earn greater professionalism and expertise in the current system is problematic after the current episodes of this worldwide economic meltdown where companies such as AIG, Lehman Brothers, and Goldman Sachs fell. This was once it forced a charge of $2.6 million to repay a class-action lawsuit assaulting wrong insurance sales clinics in 1997 and a $65 million dollar fine out of state insurance companies in 1996. AMP shut its own life surgeries to get brand new business in June 2003. Royal Sun Alliance also closed down their lucrative companies in 2002. In accordance with the Mercer Oliver Wyman Report that the German, Swiss, French and British carriers have problems with acute capital inadequacy, and it is due to job risky investments in debt and equity instruments previously. Thus FDI at Insurance in India will introduce our monetary markets into the suspicious and insecure activities of their foreign exchange businesses at some period once the merits of controlling such activities happen to be discussed at the advanced nations.

3. Greater channelization of economies to insurance: Among the very crucial duties played with the insurance industry would be to segregate federal savings and divides them to investments in various industries of their market. But, no substantial change appears to have happened up to mobilizing economies by the insurance industry is worried even following the liberalization of the insurance industry in 1999. For that reason, the foreign or private involvement have been able to get the aim.

4. The flow of capital to infrastructure: The key aim of the life insurance plan is all about devoting the economies to the evolution of the market in long-term investment in social and infrastructure businesses. The exact same vision was contended because of its opening of insurance market would empower a substantial stream of capital into infrastructure. However, a lot more than fifty% of those coverages that they sell are ULIPS at which the investments get in the equity markets. Under those strategies, not quite 50 percent of that capital is spent in stocks hence limiting the finance accessibility for property investments. IRDA figures suggest that the talk of their public industry life and non-life insurers in investment in infrastructure is significantly higher compared to their market share. In spite of the FDI limit being put in 26 percent, the investment against the insurance industry to the infrastructure industry has been mostly from the public business companies. Thus the purpose of increasing the FDI cap in the insurance industry for mobilizing resources will not appear good.

Conclusion

The prognosis for its overall insurance company in India is stable centered on constant basic credit requirements in the industry during the next 12-18 months. With the Indian market forecast to grow at 9 percent this season and contributed rising income levels and greater hazard awareness among guaranteed, the nation's insurer is optimistic about demand for their services and products.However, before existent insurance companies reveal substantial advantages or it addresses the difficulties in hand, there might be no a lot of importance accession to this nation.

Comments

Post a Comment